Understanding Anti-Money Laundering in Real Estate

Anti-Money Laundering refers to the body of rules and procedures designed to stop criminals from successfully converting illegally obtained funds into assets that look, on paper, entirely legitimate. The objective is straightforward: keep money derived from fraud, corruption, trafficking, and similar crimes from finding its way into the legitimate financial system, and real estate has become one of the sectors most exposed to that risk.

Money laundering typically moves through three stages. Placement introduces illegal cash into the financial system, often through deposits, property payments, or large cash purchases. Layering then obscures the money’s origin through a deliberately complex chain of transfers, multiple accounts, and offshore entities. Integration completes the cycle once the funds appear “clean” and are used to acquire assets — real estate, businesses, or luxury goods — that give the money a legitimate-looking source.

Real estate firms, banks, and brokers are expected to apply Know Your Customer checks, Customer Due Diligence, risk assessment, transaction monitoring, and suspicious activity reporting precisely because property transactions routinely involve the kind of high-value sums that make all three stages — particularly integration — easy to disguise.

The Legal Framework Governing AML in the UAE

The UAE’s AML regime has been substantially rebuilt in recent years, and businesses relying on older guidance should be aware of exactly what changed. Federal Decree-Law No. 10 of 2025, effective from 14 October 2025, repealed the previous Federal Decree-Law No. 20 of 2018 in its entirety. The implementing regulation followed shortly after: Cabinet Resolution No. 134 of 2025, effective from 14 December 2025, replaced the earlier Cabinet Decision No. 10 of 2019.

This wasn’t a routine refresh. The 2025 framework lowered the evidentiary threshold for establishing liability — knowledge of a transaction’s illicit origin can now be inferred from objective circumstances rather than requiring direct proof — expanded the scope of regulated activity to bring virtual asset service providers within reach, and introduced proliferation financing as a standalone offence alongside money laundering and terrorism financing.

Oversight of the real estate sector specifically sits across several bodies: the Ministry of Economy, the Financial Intelligence Unit (FIU), sector regulators including the Dubai Land Department, and broader guidance from the Financial Action Task Force (FATF), whose evaluation standards continue to shape how aggressively UAE authorities enforce these rules.

Need Expert Advice?

Contact the team at Farahat & Co. for professional support and expert insights for businesses operating in the UAE.

Real Estate as a Designated Non-Financial Business and Profession

Real estate agents, brokers, developers, and property managers fall within the category of Designated Non-Financial Businesses and Professions (DNFBPs) under UAE law — a classification carrying specific, binding obligations:

- Verifying clients before completing any property transaction

- Identifying the Ultimate Beneficial Owner (UBO) behind any corporate or trust structure involved

- Applying a genuinely risk-based approach rather than a uniform check applied identically to every client

- Monitoring transactions for unusual or high-risk patterns

- Reporting suspicious activity through the goAML platform

- Retaining records for a minimum of five years

Failing to meet these obligations carries serious consequences — substantial fines, licence suspension or cancellation, and in serious cases, criminal liability for the individuals involved.

Why AML Compliance Matters So Much for Real Estate Professionals

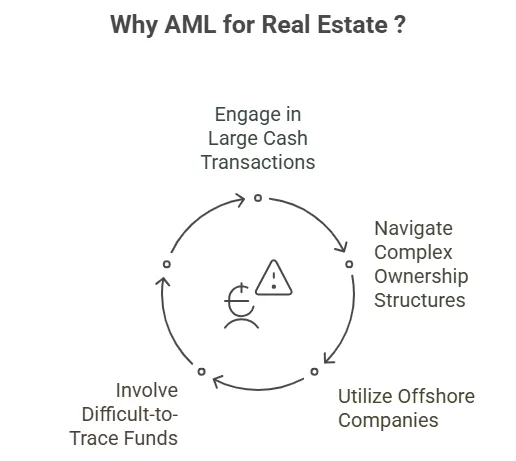

Real estate is consistently one of the most attractive sectors for money launderers, and the reasons are structural rather than incidental. Properties can be purchased with large cash sums, acquired through deliberately complicated ownership structures, funded through offshore companies, or paid for with money that’s genuinely difficult to trace back to its source. Criminals routinely buy and sell property specifically to convert illegal proceeds into something that looks like a legitimate capital gain.

For real estate professionals, AML compliance matters for reasons that go beyond simply avoiding a fine. It is a binding legal requirement under UAE law, and non-compliance can mean financial penalties, licence suspension, or criminal charges. Beyond the legal exposure, proper compliance protects a firm’s reputation, reduces the risk of unintentional involvement in someone else’s criminal activity, and builds the kind of transparency that genuinely matters to foreign investors deciding where to place their capital.

How Money Laundering Actually Happens in Real Estate

Understanding the specific mechanics helps explain why the compliance obligations above are structured the way they are.

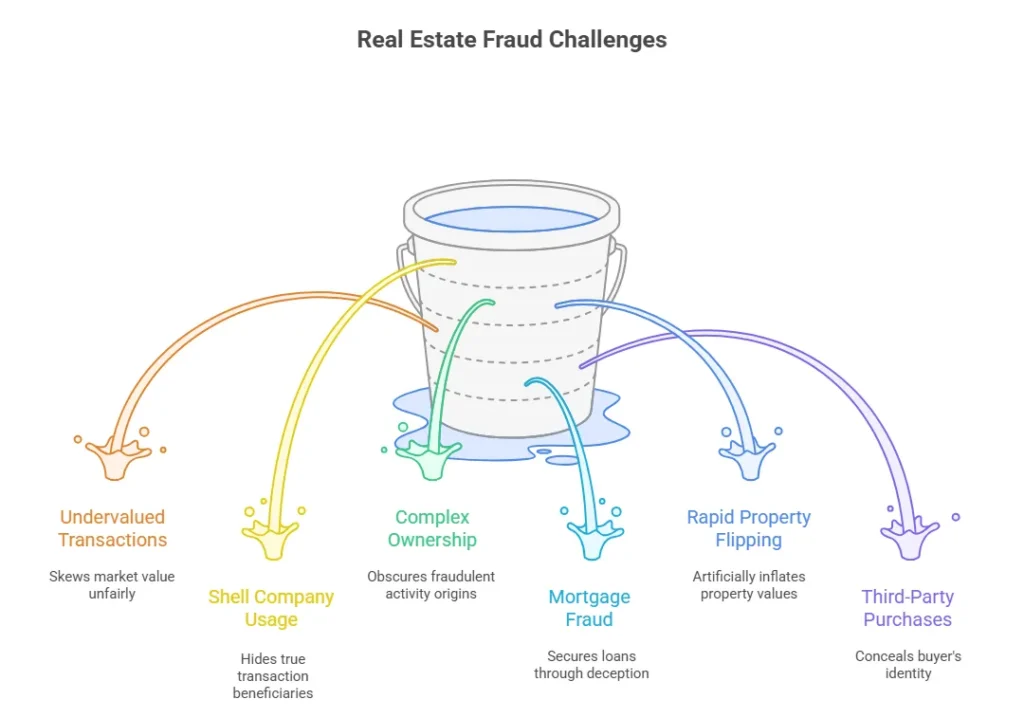

- Cash purchases — large cash payments are inherently difficult to trace back to their original source

- Under- or over-valued transactions — properties priced below market value can conceal illicit funds, while inflated valuations can manufacture a fictitious profit

- Shell companies — entities with no genuine operations, used specifically to obscure the real owner of an asset

- Complex ownership structures — trusts, offshore entities, and multi-layered corporate chains designed to hide the true UBO

- Mortgage fraud — forged income documentation, sometimes involving collusion with third parties

- Rapid property flipping — buying and reselling quickly to move large sums through the system with minimal scrutiny at each step

- Third-party purchases — using someone else’s name on the transaction to put distance between the criminal and the asset

Red Flags Worth Particular Attention

- Unusual or unexplained cash payments

- Sudden interest in luxury properties without a clear financial profile to support it

- Buyers connected to high-risk jurisdictions

- Clients who resist or refuse standard identification requirements

- Unusually quick resale of a recently purchased property

- A mismatch between a client’s declared income and the value of the property in question

Why Dubai’s Real Estate Market Faces Particular AML Exposure

Dubai’s property market carries a specific combination of features that draw heightened AML attention: genuinely high-value transactions, a large base of international buyers, significant cross-border capital flows, and a pace of growth that can outstrip the speed of routine due diligence if firms aren’t disciplined about it. In response, UAE authorities have continued tightening AML controls specifically to safeguard market integrity, keep illicit funds out of the market, align with FATF standards, and protect the UAE’s broader reputation as a stable, transparent economy.

Real estate companies operating in this environment need to maintain genuine discipline around Customer Due Diligence, source-of-funds verification, suspicious activity reporting, proper record-keeping, and confirming that the ownership structures behind a transaction are actually legitimate rather than simply plausible.

Best Practices for Real Estate AML Compliance

A Genuine Risk-Based Approach

Every client and transaction should be assessed against its actual risk level, with materially stronger checks applied to higher-risk relationships rather than a single, uniform process applied identically across the board.

Appointing a Qualified Compliance Officer

A trained Compliance Officer should oversee document review, staff training, and the escalation of any AML or CFT concerns. Under the current legal framework, accountability for this role attaches personally to the individual holding it, not solely to the firm.

Strong Internal Controls

An effective AML policy manual should cover internal procedures, customer verification standards, transaction monitoring, clear escalation steps, and the practical mechanics of reporting through goAML.

Customer Due Diligence

Real estate agents, developers, and brokers need to verify client identities, complete standard KYC checks, identify the Ultimate Beneficial Owner, understand the source of funds involved, and apply Enhanced Due Diligence specifically where a client presents a higher risk profile.

Record-Keeping

All supporting documentation — identification records, contracts, payment receipts, and CDD files — should be archived for at least five years, available on demand if a regulator requests it.

Mandatory Reporting

Companies must submit Suspicious Transaction Reports (STRs), Suspicious Activity Reports (SARs), and Real Estate Activity Reports (REARs) through the UAE’s Financial Intelligence Unit as required.

How AML Rules Affect Foreign Investors

Foreign buyers make up a significant share of the UAE real estate market, and AML rules exist partly to keep that market genuinely safe for them — verifying overseas funds, maintaining transparency, and protecting legitimate investors from exposure to financial crime they had no part in. In practice, foreign buyers may face additional checks where they’re identified as politically exposed persons, extra documentation requirements where they’re transacting through offshore companies or trusts, and a need to confirm the legitimate source of their funds before a transaction can proceed. These steps, while sometimes experienced as friction, are part of what sustains confidence in the UAE as a stable, well-regulated market over the long term.

Consequences of Non-Compliance

AML compliance in UAE real estate is not optional. Firms that fail to meet their obligations can face heavy financial penalties, licence suspension or revocation, criminal liability — including the possibility of imprisonment for responsible individuals — and serious, often lasting reputational damage. For agents, brokers, and developers, proper compliance instead delivers safer transactions, protection from inadvertent exposure to high-risk clients, stronger investor trust, and a more transparent, healthier market overall.

How Government Bodies Coordinate AML Enforcement in Real Estate

AML enforcement in the real estate sector draws on coordination across several authorities — the Ministry of Justice, the Ministry of Economy, and the Dubai Land Department among them — working together to enforce federal AML/CFT law, monitor suspicious property transactions, regulate property transfers, and oversee the lawyers, notaries, and legal consultants involved in property dealings. This coordinated structure is part of what gives the UAE’s broader AML framework its practical reach across the full chain of a real estate transaction, not just the point of sale itself.

What an AML Audit Actually Involves

An AML audit is an independent review of a company’s AML program, assessing whether its policies and procedures are genuinely effective, whether staff actually follow the required compliance steps in practice, whether the company meets its legal obligations, and where any weaknesses or gaps exist. A typical audit examines risk assessment processes, CDD procedures, monitoring controls, staff training programs, STR/SAR reporting practices, and record-keeping systems.

Audits are generally performed by recognized third-party firms, independent auditors, or certified AML professionals, with frequency shaped by regulatory requirements, company size, and overall risk level — most firms complete a full audit on an annual or biennial basis. The benefits compound over time: improved compliance, lower exposure to fines, a stronger reputation with regulators and clients, and genuinely better operational controls.

Frequently Asked Questions (FAQs)

What is anti-money laundering compliance for real estate businesses?

It refers to the full set of measures a real estate business takes to prevent property transactions from being used to launder illicit funds, including Know Your Customer checks, Customer Due Diligence, suspicious activity reporting, and proper record-keeping.

Why does AML matter specifically in the real estate sector?

Real estate involves high-value transactions, making it an attractive target for laundering illicit funds. AML compliance protects the property market from being exploited for this purpose and protects firms from legal and reputational exposure.

How does money laundering typically happen in real estate?

Common methods include large cash purchases, the use of shell companies, under- or over-valued transactions, complex offshore ownership structures, and the rapid resale of properties to move funds through the system quickly.

What are the current AML requirements for real estate businesses in the UAE?

Under Federal Decree-Law No. 10 of 2025 and Cabinet Resolution No. 134 of 2025, real estate businesses must perform KYC and CDD checks, identify the Ultimate Beneficial Owner, report suspicious activity through goAML, retain records for at least five years, and apply ongoing transaction monitoring.

Who is considered a DNFBP in the UAE real estate sector?

Real estate brokers, developers, agents, and property managers engaged in the sale or purchase of property are classified as Designated Non-Financial Businesses and Professions under UAE AML law.

How often should real estate companies in Dubai conduct an AML audit?

Most firms conduct a full AML audit annually or biennially, with the appropriate frequency depending on the company’s risk profile, size, and applicable regulatory requirements.

What penalties apply for non-compliance with AML regulations in UAE real estate?

Penalties can include substantial financial fines, licence suspension or cancellation, and criminal liability, including potential imprisonment for individuals found responsible.

Need Expert Advice?

Contact the team at Farahat & Co. for professional support and expert insights for businesses operating in the UAE.

How Farahat & Co. Can Help

Farahat & Co. supports real estate brokers, developers, and property managers across the UAE with AML compliance — from developing internal policies and CDD workflows through to goAML registration, independent AML audits, staff training, and ongoing compliance support aligned with the current legal framework.

Contact Farahat & Co. today to strengthen your real estate firm’s AML compliance.

{kind=link}