UAE e-invoicing is now an active compliance preparation project, not a distant concept. The Ministry of Finance has already published the framework, pilot, and voluntary onboarding start on 1 July 2026, the ASP appointment deadline for large businesses has been extended to 30 October 2026, and mandatory implementation begins in phases from 1 January 2027, depending on revenue and entity type. For UAE businesses, the real issue is not only whether an invoice can be generated electronically. It is whether the business can issue, receive, map, validate, store, and reconcile structured invoice data in a way that fits VAT rules, accounting records, audit evidence, and future FTA review. That is why businesses should treat 2026 as a preparation window for systems, data, controls, and documentation, and not wait for a mandatory date to discover internal gaps.

☰ Table of Contents

- UAE E-Invoicing Rollout Timeline

- What UAE E-Invoicing Means in the UAE

- Who Should Prepare Now

- Why It Matters Before 2027

- Authority Rule vs Business Reality

- UAE E-Invoicing Readiness Checklist Before 2027

- Documents and Records to Review Before Onboarding

- Common Mistakes Businesses Make

- Risks, Penalties, and Delays

- Short Practical Scenarios

- When to Seek Professional Help

- How Farahat & Co. Can Assist

- FAQs

Quick Summary

- Who is affected? Any person conducting business in the UAE is within scope unless specifically excluded, and the business-facing scope covers B2B and B2G transactions. Consumer transactions are generally outside scope.

- What is required? Businesses in scope must work through a UAE Accredited Service Provider, exchange structured electronic invoices, and report invoice data through the UAE e-invoicing system.

- What is the main risk? The risk is not only administrative fines. It is also bad master data, failed validation, VAT mismatches, weak audit trails, and delayed corrections after go-live. The penalty framework for mandatory entities is already published.

- What should businesses do next? Confirm implementation timing, identify in-scope transaction types, review master data, choose an ASP from the Ministry’s list, and test invoice-to-ledger-to-VAT workflows before mandatory onboarding.

- Relevant Farahat & Co. support: UAE e-invoicing advisory and compliance support, VAT consultancy services, and accounting and bookkeeping services can help businesses review readiness from both tax and records perspectives.

UAE E-Invoicing Rollout Timeline

| Category | ASP Appointment Deadline | Mandatory Implementation Date |

| Revenue of AED 50 million or more | 30 October 2026 | 1 January 2027 |

| Revenue below AED 50 million | 31 March 2027 | 1 July 2027 |

| Government entities | 31 March 2027 | 1 October 2027 |

Need Expert Advice?

Contact the team at Farahat & Co. for professional support and expert insights for businesses operating in the UAE.

What UAE E-Invoicing Means in the UAE

In the UAE, an electronic invoice is not just a PDF sent by email. The Ministry of Finance describes e-invoicing as a structured electronic format that allows automatic processing, and earlier programme material expressly says that PDF, Word, image files, scanned invoices, and unstructured HTML invoices are not e-invoices. The UAE model uses a Decentralized Continuous Transaction Control and Exchange (DCTCE) / 5-corner model, with invoice exchange through accredited service providers and tax data reporting to the FTA.

For a real business, that means invoice compliance is moving away from “does the document show the required text?” toward “is the underlying transaction data complete, correctly classified, technically mapped, and consistently reportable across systems?” That change affects finance, procurement, billing, ERP, VAT review, and document retention at the same time.

Who Should Prepare Now

The scope is broader than many businesses expect. The official guidance states that all persons who make a business transaction in the UAE are within scope, regardless of VAT registration status, unless specifically excluded. The business-facing transaction matrix shows B2B and B2G in scope, while supplies made to consumers are generally out of scope. Goods and services supplied to government entities are also specifically brought into scope.

That means preparation is relevant for many types of UAE businesses, including:

- mainland companies selling to other businesses or government entities,

- free zone companies, including businesses with free zone counterparties or free zone transaction flags,

- branches of foreign companies,

- trading, import/export, and distribution businesses,

- professional services firms using milestone or continuous billing,

- e-commerce businesses with B2B sales channels,

- businesses below the VAT registration threshold today but still conducting business transactions that may later fall into the e-invoicing rollout, and

- government suppliers that depend on tender or procurement documentation.

Important exclusions

Not every transaction is treated the same way. Exclusions include certain sovereign government activity, certain airline passenger-related documents, a temporary exclusion for certain airline goods transport documents, and specified financial services that are exempt from VAT or zero-rated under the VAT Executive Regulation. Businesses should therefore review both entity scope and transaction scope, not assume that one answer covers the whole business.

Why It Matters Before 2027

The Ministry of Finance says e-invoicing will support invoice tax data reporting to the FTA, help pre-populate certain VAT return fields, and expedite refund processing. That makes this a tax process issue, not only an IT project. If invoice data is incomplete or incorrectly coded, the problem may surface later in VAT returns, refund support, audit trails, or financial statement reconciliations.A second practical point is timing. The pilot and voluntary phase start on 1 July 2026, while businesses with annual revenue of at least AED 50 million now have until 30 October 2026 to appoint an Accredited Service Provider. Mandatory implementation still begins from 1 January 2027 for persons with annual revenue of at least AED 50 million, from 1 July 2027 for persons below that threshold, and from 1 October 2027 for government entities. Businesses that wait until their mandatory date may leave too little time for data cleanup, ASP onboarding, system testing, counterpart communication, and control design.

Compliance Note

The voluntary phase should not be treated as “nothing applies yet.” A business that chooses to onboard voluntarily from 1 July 2026 must still follow the technical requirements of the UAE system, even though administrative penalties only apply from its mandatory date.

Authority Rule vs Business Reality

- Official rule: An e-invoice must be structured and machine-processable.

Business reality: A clean PDF template alone does not solve readiness. The business needs correct fields, identifiers, mappings, and exchange capability. - Official rule: Scope is not limited to VAT-registered persons.

Business reality: Businesses should not assume “no TRN, no action.” Master data, transaction type, and future onboarding timing still need review. - Official rule: One ASP must cover both sending and receiving electronic invoices.

Business reality: Sales, accounts receivable, procurement, and accounts payable cannot plan separately. Vendor selection is a cross-functional decision. - Official rule: Mandatory rollout is phased by revenue and entity type.

Business reality: 2026 is the window to test and correct. It is not a safe reason to delay all readiness work. - Official rule: Customer onboarding status does not remove the supplier’s obligation.

Business reality: During transition, businesses must think about counterpart readiness, fallback workflows, and how invoices will still be issued correctly when not every buyer is onboarded yet.

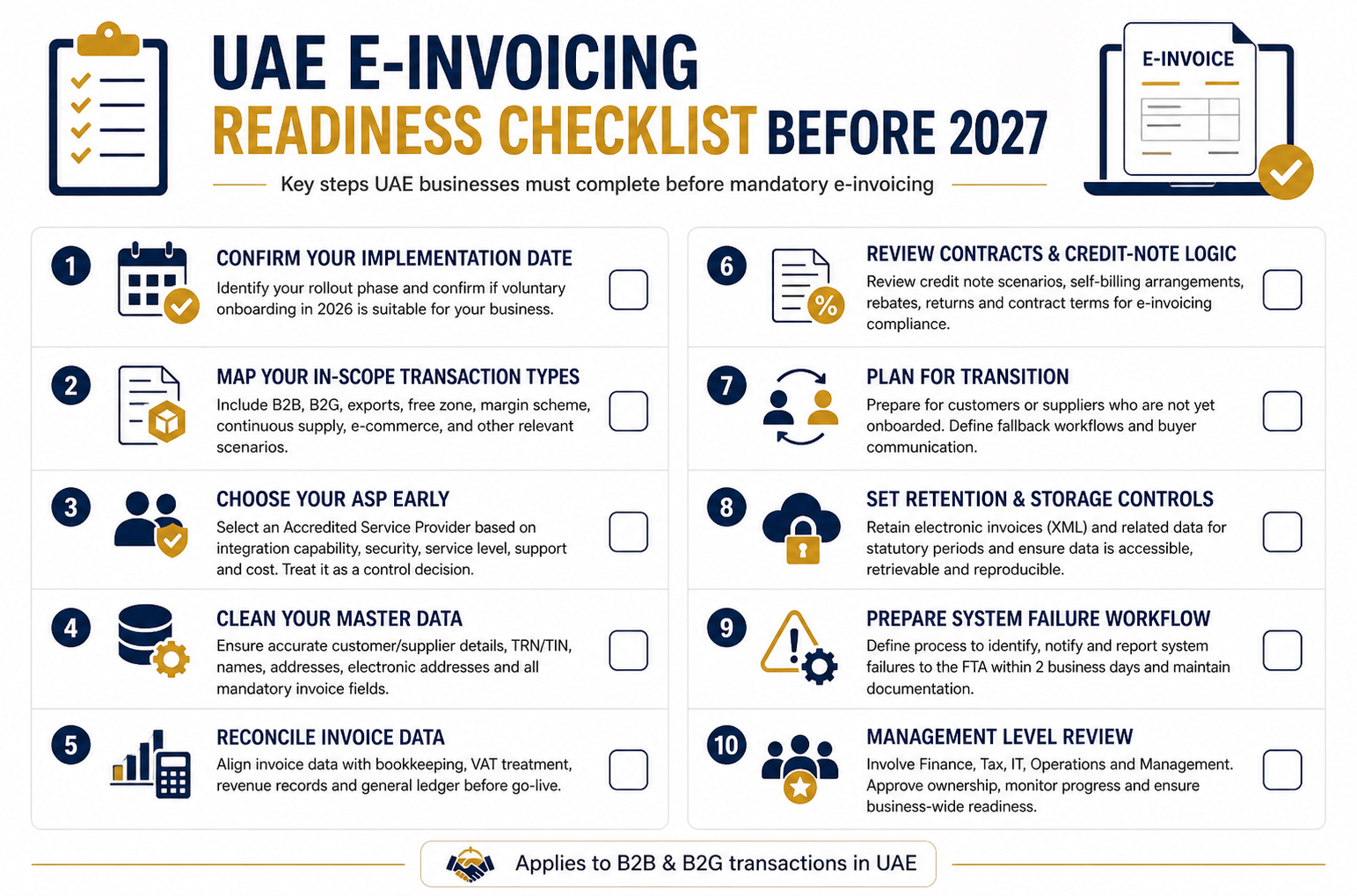

UAE E-Invoicing Readiness Checklist Before 2027

1) Confirm your implementation date and whether you should use the voluntary phase

Start by identifying which rollout phase the business falls into and whether voluntary onboarding in 2026 is useful. Large businesses with annual revenue of at least AED 50 million have the earliest mandatory dates, but smaller businesses may still benefit from voluntary onboarding to test their environment without mandatory-phase penalty exposure. Also confirm whether the business has B2G supplies, because government-facing transactions should not be ignored during readiness planning.

2) Map your in-scope transaction types, not just your legal entity

The mandatory fields guidance shows that UAE e-invoicing is not a single-format exercise. Transaction logic must distinguish scenarios such as free trade zone, deemed supply, margin scheme, summary invoice, continuous supply, disclosed agent billing, supply through e-commerce, and exports. If your ERP or invoicing process does not identify those scenarios correctly, the invoice may be technically incomplete or commercially misleading.

What this means in practice

A business should review its transaction universe by scenario, not only by department. A services company may need special handling for retainers and milestones. A trading company may need export and free zone logic. An e-commerce seller may need a distinct workflow for platform data. A disclosed-agent structure may require invoice rules that differ from ordinary billing.

3) Choose your ASP early and treat it as a control decision, not only a procurement decision

The Ministry requires businesses to appoint an Accredited Service Provider, and the Ministry also publishes the current list of pre-approved providers, which is updated periodically. Its own selection guidance suggests reviewing integration capability, data residency, security, service levels, pricing structure, and support arrangements. The guidance also recommends ensuring that the ASP contract includes 100 free electronic invoices per annum.

This decision should involve finance, tax, IT, and operations. A technically good vendor may still be the wrong fit if it cannot integrate cleanly with your ERP, does not support exception handling well, or leaves the business dependent on a subcontracted support chain during live issues.

4) Clean your master data before you start testing

The UAE mandatory fields go beyond basic invoice heading information. Required fields include invoice number, invoice date, invoice type code, currency code, payment due date, transaction type code, seller and buyer names, electronic addresses, identifiers, tax identifiers, address fields, totals, tax breakdown, and line-level details. For VAT-registered parties, TRN/TIN-related fields matter.

Documentation Note

Many businesses understand VAT invoice content at a high level, but e-invoicing readiness often fails at the master-data level: outdated customer names, inconsistent trade license details, missing electronic addresses, wrong registration identifiers, or poor mapping between legal entity and billing entity. Those issues can delay onboarding even when invoice templates look correct on paper.

5) Reconcile invoice data with bookkeeping, VAT, and revenue records

E-invoicing should not sit outside the accounting system. Businesses should test whether invoice totals, VAT codes, credit notes, and timing align with the general ledger, VAT return logic, and revenue recognition process. The Ministry has also made clear that e-invoicing does not remove VAT tax invoice obligations; rather, the electronic invoice must satisfy the VAT tax invoice requirements where applicable.

This is where a pre-go-live VAT compliance review VAT compliance review and VAT return filing and accounting support can be especially useful, because the larger risk is often not the first invoice itself but the mismatch between invoicing data, VAT treatment, and posted accounting entries.

6) Review contracts, credit-note logic, and self-billing arrangements

Ministerial Decision No. 243 of 2025 requires electronic credit notes where a transaction is cancelled, consideration is reduced, the amount is returned, or an administrative or numerical error occurred. The guidelines also explain that self-billing is only available in certain VAT contexts and that businesses should review self-billing arrangements because the buyer may not be in mandatory scope at the same time as the supplier.

Tax Review Point

This requirement should not be treated as a simple format change. It may affect contract wording, approval matrices, rebate arrangements, return policies, and how the business documents output tax adjustments. If those underlying records are weak, the tax position may still be questioned later even if the invoice file itself is technically valid.

7) Plan for transition where customers or suppliers are not all onboarded

The official guidance says a customer’s onboarding status does not affect the supplier’s obligation. It also explains that when issuing tax invoices to buyers that have not yet implemented e-invoicing, a regular tax invoice such as PDF may still be required in addition to the electronic tax invoice during transition, and a predefined endpoint must be used where the buyer has not yet implemented and does not have a participant identifier.

That means businesses should not assume a simple “all counterparties will switch together” scenario. Readiness should include buyer communications, onboarding status tracking, fallback document workflows, and testing across real counterpart categories.

8) Set up retention, storage, and retrieval controls properly

The guidelines say electronic invoices are issued, transmitted, and received in XML format, and data relating to issuance, transmission, and receipt must be retained for statutory periods. The guidance states 5 years for taxable persons following the relevant tax period, 5 years for non-taxable persons from the end of the relevant calendar year, and 7 years for real estate records, with additional periods in certain disputes, audits, or voluntary disclosure situations. It also clarifies that “within the State” should be read functionally: the key issue is whether records and associated data remain accessible, reproducible, and retrievable for the FTA when requested.

Farahat & Co. Insight

Businesses should not reduce this to a cloud-location discussion alone. The real control question is whether the business can produce a complete invoice record, related audit trail, and supporting data promptly when needed. That affects IT architecture, document policy, internal access rights, and audit readiness.

9) Create a system-failure and exception workflow before go-live

The law requires issuers and recipients to notify the FTA of a system failure within 2 business days. The penalty resolution then imposes AED 1,000 per day or part thereof for failure to notify on time. This is a strong sign that exception management needs to be designed in advance, not improvised later.

A practical workflow should define who identifies the issue, who assesses whether it is a reportable system failure, who contacts the ASP, who notifies the authority, what interim billing control applies, and how the incident is documented for future review.

10) Treat readiness as a management review item, not only a finance task

The official model touches billing, purchasing, tax reporting, invoice exchange, data security, and record retention. For that reason, management should review readiness across functions, approve ownership, and monitor milestones before onboarding. Businesses with free zone activity, exports, related-party transactions, or complex contract structures should not leave the review only to one finance user or one software vendor.

Documents and Records to Review Before Onboarding

A useful readiness file usually includes:

- trade license and legal entity details,

- seller and buyer master data, including names, identifiers, and address fields,

- TRN/TIN details where applicable,

- invoice numbering logic and payment due date logic,

- tax code mapping and line-level VAT treatment,

- contracts, purchase orders, and credit-note approval support,

- free zone, export, agent, e-commerce, or continuous-supply transaction flags,

- ERP/accounting/invoicing system mapping documents,

- ASP agreement, implementation plan, and test logs,

- retention and retrieval policy for electronic invoice data,

- incident and system-failure escalation procedures, and

- reconciliation reports tying invoices to the ledger, VAT returns, and management reporting.

This is also a good stage to review whether your accounting and bookkeeping services setup is producing consistent, audit-ready transaction data rather than only year-end summaries.

Common Mistakes Businesses Make

Many businesses understand the basic rule but apply it incorrectly because they do not review the supporting records behind the invoice process. Common problems include:

- treating PDF invoices as “e-invoicing ready,”

- assuming the issue only concerns VAT-registered entities,

- focusing on sales invoices but ignoring accounts payable and recipient-side processing,

- delaying ASP selection until the mandatory deadline is close,

- failing to map special transaction types such as e-commerce, continuous supply, exports, or free zone activity,

- ignoring credit-note workflows and self-billing contracts,

- assuming e-invoicing replaces ordinary VAT, accounting, or audit documentation, and

- not preparing a system-failure escalation process.

Risks, Penalties, and Delays

The Ministry of Finance has already announced the administrative fine framework for mandatory entities. Published examples include:

- AED 5,000 per month for failing to implement the e-invoicing system or failing to appoint an approved service provider within the required timeframe,

- AED 100 per electronic invoice not issued or sent on time, capped at AED 5,000 per month,

- AED 100 per electronic credit note not issued or sent on time, capped at AED 5,000 per month, and

- AED 1,000 per day or part thereof for failing to notify the FTA of a system malfunction within the specified timeframe.

The bigger issue, however, is often not the penalty itself. In practice, the larger exposure may be delayed corrections, manual workarounds, inconsistent records, refund complications, buyer disputes, and future authority scrutiny if invoice data does not align with the accounting and tax file.

Short Practical Scenarios

Trading company with imports and exports

A trading company may need export flags, customs alignment, buyer master-data cleanup, and free zone logic where relevant. If shipping, inventory, and invoice data are held in separate systems, reconciliation should be tested before onboarding.

Professional services firm with retainers and milestone billing

A service provider with monthly retainers, milestone billing, or retention amounts should review continuous-supply handling, due-date logic, and credit-note workflows. The invoice file may be simple, but the tax point and adjustment logic may not be.

E-commerce seller sending platform-generated PDFs

A platform PDF may look complete to the customer, but PDF alone is not a UAE e-invoice. The seller still needs structured invoice data, correct transaction-type handling, and exchange/reporting capability through the UAE model.

Supplier to a government entity

A business dealing with government tenders or procurement portals should treat B2G readiness as a priority. Government supplies are in scope, and late planning can disrupt billing, acceptance, and public-sector cash-flow timing.

Farahat & Co. Review Perspective

From a tax and records review perspective, the key question is not only whether the business understands the e-invoicing framework. It is whether the invoice position is supported by the accounting records, contracts, credit-note logic, customer and supplier data, VAT treatment, and document retention setup behind it.

From an audit perspective, businesses may have invoices and bank records but still face readiness issues if transactions are not classified consistently, exceptions are not documented, or the ledger does not reconcile back to the invoice data that will flow through the UAE model. That is why e-invoicing preparation often overlaps naturally with audit services in UAE, VAT review, and records remediation.

When to Seek Professional Help

A business should seek professional advice when the matter involves:

- unclear VAT treatment,

- free zone or export transactions,

- large invoice volumes,

- related-party transactions that also affect corporate tax advisory,

- incomplete customer or supplier data,

- credit-note or self-billing complexity,

- FTA notices or existing penalty exposure,

- weak bookkeeping or reconciliation gaps,

- system changes across ERP, billing, and procurement, or

- a need to align e-invoicing with audit readiness and transaction traceability.

In these cases, the issue is usually not limited to understanding the rule. It also requires reviewing records, documents, system logic, contracts, and business facts before the company goes live.

How Farahat & Co. Can Assist

Farahat & Co. assists UAE businesses with e-invoicing readiness by reviewing applicable requirements, assessing invoice and master-data quality, checking VAT and bookkeeping alignment, supporting documentation design, identifying control gaps, and helping management understand the right next step.

Depending on the business, that support may include UAE e-invoicing advisory and compliance support, VAT registration services, VAT consultancy services, VAT return filing and accounting support, and accounting and bookkeeping services, where transaction traceability and control documentation need review. Our aim is to help businesses approach onboarding with clearer records, better coordination, and less avoidable correction work later.

Expert Comment from Farahat & Co.’s VAT & Indirect Tax Advisory Department

“The businesses most likely to struggle with UAE e-invoicing are not always the ones with the oldest software. The more common issue is fragmented data across sales, finance, tax, procurement, and customer master files. If those records do not align before onboarding, the invoice may pass through a system but still create VAT, accounting, or audit risk later.”

Author

M. A Farahat, ACPA , CFE , CICA

Senior Consultant

Regulated Tax Agent in UAE

Regulated Court Expert Witness in UAE

Need Expert Advice?

Contact the team at Farahat & Co. for professional support and expert insights for businesses operating in the UAE.

FAQs

Is UAE e-invoicing mandatory?

Yes, the UAE has already issued the framework and implementation decisions. Pilot and voluntary onboarding begin on 1 July 2026. Mandatory onboarding is phased: persons with annual revenue of at least AED 50 million from 1 January 2027, persons below that threshold from 1 July 2027, and government entities from 1 October 2027. Businesses with annual revenue of at least AED 50 million must appoint an Accredited Service Provider by 30 October 2026.

Does UAE e-invoicing apply only to VAT-registered businesses?

No. The official guidance says all persons making a business transaction in the UAE are within scope regardless of VAT registration status, unless specifically excluded. VAT registration status still matters for some invoice categories and fields, but it is not the only scope test.

Are PDF invoices enough for UAE e-invoicing?

No. UAE programme materials state that PDF, Word, image files, scanned invoices, and unstructured HTML are not e-invoices. The system requires structured electronic data that can be processed automatically.

Does it apply to free zone companies?

Yes, free zone activity can be relevant, and the UAE mandatory fields specifically include transaction-type logic for free trade zone scenarios. A free zone company should not assume it is outside the framework simply because it operates in a free zone.

What records matter most before onboarding?

The priority records are legal entity and customer/supplier master data, TRN/TIN fields where applicable, invoice and tax-code mapping, transaction-type flags, ASP contract details, reconciliation reports, and document-retention controls. Those records determine whether the invoice can be issued accurately and supported later.

What happens if a system failure occurs?

The issuer and recipient must notify the FTA of a system failure within 2 business days in the manner determined by the authority. The published fines include AED 1,000 per day or part thereof for late notification.

Does e-invoicing replace VAT invoice rules?

No. The guidance expressly says e-invoicing requirements are different from VAT tax invoice requirements. For taxable supplies, the electronic invoice still needs to satisfy the VAT tax invoice framework where applicable.

Can Farahat & Co. help with readiness before the mandatory phase?

Yes. Farahat & Co. supports businesses with e-invoicing readiness review, VAT alignment, bookkeeping cleanup, audit-ready records, and related compliance support so the business can prepare before the mandatory phase rather than correct issues after go-live.

{kind=link}